How people will game Obamacare

When I was in my twenties I thought I was invincible and would live forever. I was wrong. I now know that I’m not invincible, and definitely won’t live forever. I know better now, but if you’re twenty-something you don’t believe it. You will, sooner or later.

I am disturbed by Obamacare, not because it would be nice for uninsured people not to visit the Emergency Room when they get sick. Visiting the ER is a horrendously expensive way of receiving care, not paid for by the care recipients. As an example Georgia has about ~1.7 million uninsured residents.

What I object to is that the taxpayers will bear the financial burden of providing insurance for people who choose not to, or can’t afford to buy it. For low income buyers the taxpayers will subsidize them through Medicaid (and credits), and as they will probably buy the cheapest Bronze coverage, again later.

I read through a summary of the legislation, rather than the ~2,500 pages of the law/citations and spotted an immediate flaw. In practice it may not be, as after the bill was passed and signed into law the regulators started to write regulations as to what the law means. This may take decades. That means the Congress passed a massive, unread (by most) bill without knowing what it meant as well! I’m shocked.

Those regulations number ~30,000 pages and are increasing every week. The regulations will be subject to debate, a flurry of court cases with at least one being decided by the Supreme Court.

I immediately called my long time healthcare expert friend in San Diego. She gives webinars to insurance agents all of the time, and is considered one of the few people who really understands the law and the regulations. In other words, her words are golden.

The key dodge is that the Obamacare healthcare law allows people who have certain “life-changing events” to sign up outside of the regular yearly six-week enrollment period. One part says that if you lose your job outside of the open enrollment period, you will be able to get coverage immediately in the insurance exchanges. That’s outside of the annual open enrollment period, that this year is October 1, 2013 to March 31, 2014. Others include moving to another state or having a baby.

Further, if a person actually buys coverage they can drop it three months before year end and not receive a theoretical IRS penalty. They can buy it again during the next enrollment period. I also suspect that the insurance companies policy grace periods, before the actual cancellation date, will help the dodgers receive free coverage. In other words, if they become sick and before the cancellation date, they will promptly pay the back premiums.

The next dodge is that although penalties are collected as taxes, Congress didn’t give the IRS legal authority to actually force people to pay them, like income taxes. The IRS will be saying “please” many times and be ignored.

Even if you owe a penalty, the only way that the IRS can reasonably collect it is by deducting it from tax refunds. The gamers will make sure that they owe money by adjusting their W-4’s, so that the government won’t get interest free money until refunded the next year.

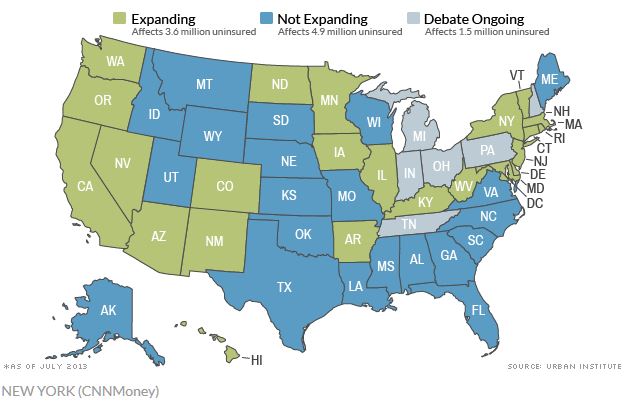

Congress also inserted a giant dodge in the legislation so that if your state doesn’t expand Medicaid as another giveaway, then for “poor adults” there aren’t any penalties! According to the Los Angeles Times the penalty waiver is valid if your individual income is no more than $46,000, or $94,000 for a family of four. These families will also get a taxpayers subsidy if they buy coverage.

The real problem with these dodges is that they will be disseminated on the Internet at the speed of light. In the past there was no way for people to expose the dodges to more than a few friends. Today it’s really easy, as everyone is your friend on Facebook. Millions will find out within seconds, by just looking on the Internet at many of the social media sites.

The real problem with these dodges is that they will be disseminated on the Internet at the speed of light. In the past there was no way for people to expose the dodges to more than a few friends. Today it’s really easy, as everyone is your friend on Facebook. Millions will find out within seconds, by just looking on the Internet at many of the social media sites.

Even large companies are using Obamacare as an excuse reason to reduce or eliminate expenses. UPS, for example, is cutting off many dependents from its medical insurance program citing Obamacare unknowns. One can only guess if this is an excuse to increase profits, or a legitimate concern.

Initially the penalty is $95 (it’s actually much higher, or 1% of family income whichever is greater) so the gamer may pay it, but as it increases it will become a game to find techniques to dodge paying. As I wrote above one easy technique is that the IRS cannot legally force compliance, so the gamer will ignore the collection letters.

So, if you don’t have insurance, and don’t want to buy it (excluding the noncollectable “tax” penalty) and become really sick, you can –

1 Wait until the next open enrollment if possible, especially if you need a non-critical surgical procedure that can wait until the next guaranteed coverage dates. You’ll buy the best Platinum coverage so your co-pay will be the least. You would obviously select Platinum to really soak the insurance companies, as it’s like choosing the winning lottery numbers after they are drawn and still receive the prize.

2 Lose your job, and be immediately eligible for (the best) Platinum coverage to pay your very expensive bills, ignoring the standard $6,350 maximum (after 2014) through all plans. I suspect that you could reapply for your job later, and get it back.

3 Quit your job, and move across state lines to be immediately eligible. Work there for a while, get your Platinum coverage and then move back.

4 Let’s forget the fourth.

Reasonably as our government is still making up the rules, so all of my observations may not be correct. I think that I’m right, and will publish more Obamacare dodges in the future.

Obamacare will prove to be the soaking of America. Let the games begin.